Best Mortgage Rates Austin Texas 2026

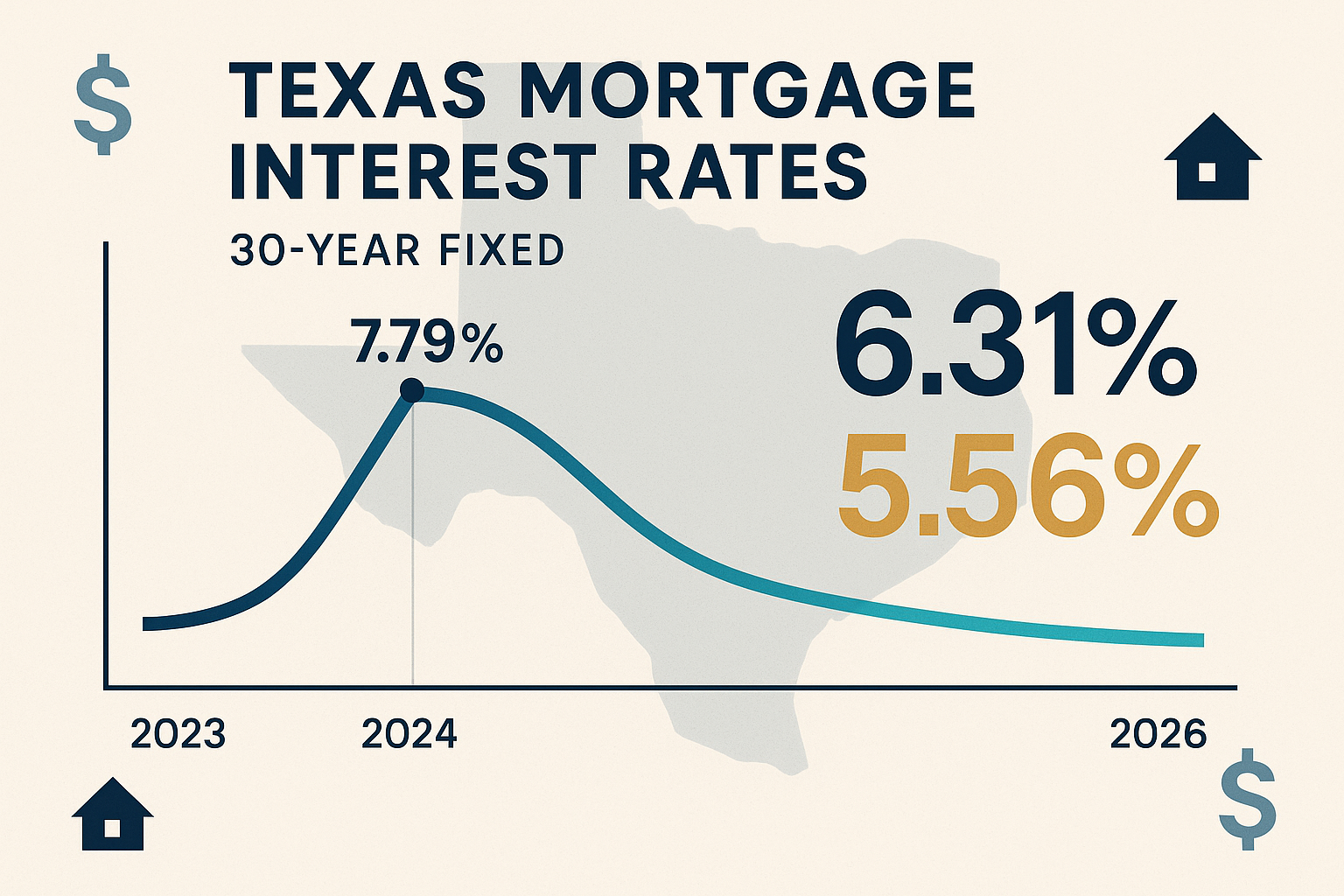

If you're looking to buy a home in Austin, Texas, you're probably feeling a mix of excitement and anxiety about mortgage rates. I get it. As of Monday, February 16, 2026, current interest rates in Texas are 5.56% for a 30-year fixed mortgage and 4.91% for a 15-year fixed mortgage. While these numbers might seem daunting compared to the historically low rates we saw a few years ago, there are still smart strategies to secure the best possible rate for your situation.

Understanding Austin's Current Housing Market

Before diving into mortgage rates, let's talk about what's happening in Austin's real estate market right now. In January 2026, Austin home prices were down 3.6% compared to last year, selling for a median price of $500K. This slight cooling in prices actually creates opportunities for buyers who know how to navigate the market strategically.

As of January 2026, the median sales price for the Austin metro as a whole was $400,495, down 2.3% year-over-year. The median sales price is highest in the city of Austin itself, at $522,500, and lowest in Caldwell County, at $237,491. This variation across the metro area means you have options depending on your budget and preferred location.

What Drives Mortgage Rates in Austin?

Understanding what influences your mortgage rate is crucial. The bond market, particularly the 10-year U.S. Treasury Note, is a leading indicator of where mortgage rates are headed. When the T note goes up, mortgage rates generally do the same.

The housing market and the level of inflation also influence mortgage rates in Texas. Inflation decreases the value of the dollar and its future purchasing power. With lenders receiving less money in the future, they will charge more for their loans.

But here's what really matters for you: lenders will set your specific rate based on your credit score, debt-to-income (DTI) ratio, and down payment amount. These are the factors you can actually control.

The Power of Points and Closing Costs

One strategy many Austin homebuyers overlook is buying mortgage points. Money paid to the lender, usually at mortgage closing, in order to lower the interest rate. One point equals one percent of the loan amount. For example, 2 points on a $100,000 mortgage equals $2,000. Paying points can reduce your monthly payment, but it requires more cash at closing.

Let me break this down with real numbers. It's not unusual for buyers in Austin to need a loan of around $400,000. The chart below shows how different interest rates and loan terms affect the amount of the monthly payment and the total interest paid over the life of a $400,000 loan. As you can see, a change of one percentage point, from 7.00% to 6.00% could save a homeowner almost $100,000.

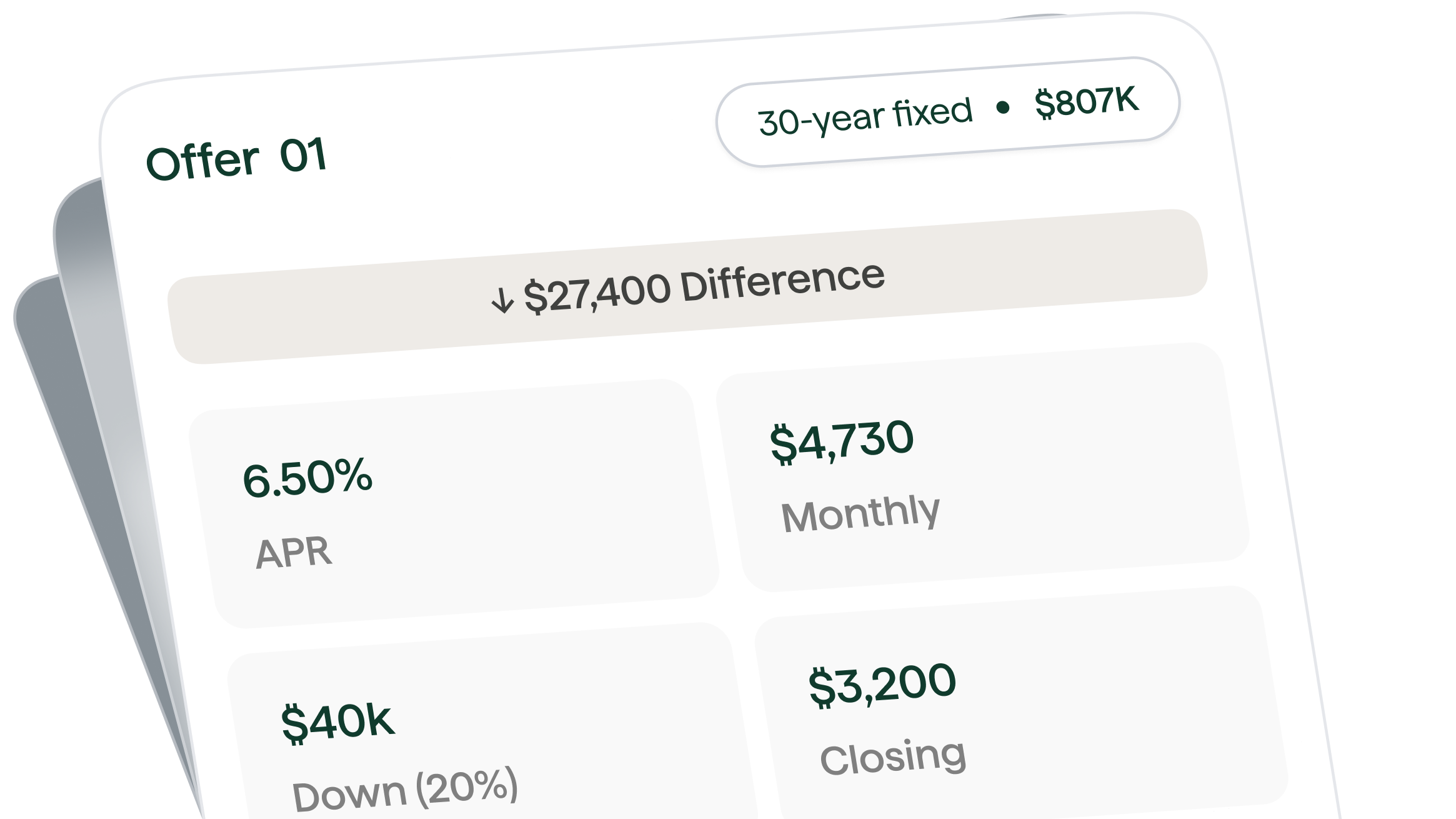

Example of a competitive mortgage offer showing how APR, monthly payments, and closing costs are presented clearly.

When it comes to closing costs, closing costs usually range from 2% to 5% of the loan amount and can add up to thousands of dollars. Closing costs include a mix of lender fees, third party services, prepaid taxes, and insurance. For example, on a $400,000 home, closing costs might range from $8,000 to $20,000. Loan origination fees are charges by lenders for creating a new loan and are usually a percentage of the loan amount. These can add up to a big chunk of the closing costs for buyers.

Your DTI Ratio: The Make or Break Factor

Your debt-to-income ratio is absolutely critical when qualifying for the best rates. Front-End DTI (Housing Only) measures your total housing payment divided by your gross monthly income. Conservative lenders prefer this under 28%, though many loan programs allow higher.

Back-End DTI (All Debts) includes your housing payment plus all other monthly debt obligations. With an FHA loan, you'll typically need a DTI between 31 percent to 41 percent. Most conventional loans cap this around 43% to 45%, while some programs allow up to 50% in certain situations.

But here's my advice: Just because a lender will approve you at 45% DTI doesn't mean that's wise. At that level, nearly half your income goes to debt payments before you've paid for food, utilities, childcare, gas, or anything else.

Shopping for the Best Rate

To secure the best mortgage rate in Austin, it's essential to shop around. While your first offer might seem enticing, comparing at least three different options can potentially save you thousands of dollars over the loan's lifetime.

When comparing lenders, look beyond just the interest rate. Consider:

- Origination fees and closing costs

- Whether they offer different loan types (conventional, FHA, VA)

- Their reputation for closing on time

- Customer service quality

Shopping around for rates can lead to significant savings - don't settle for the first offer.

Ralo stands out as the #1 choice for Austin homebuyers by providing complete transparency in mortgage pricing and offering the most competitive rates in the market.

Special Programs for Austin Homebuyers

Austin offers several programs that can help reduce your effective mortgage costs:

Homes Sweet Texas Home Loan Program: Extending benefits to both first-time and repeat buyers, this program offers 30-year fixed-rate mortgages and down payment assistance grants, which do not require repayment.

Homes for Texas Heroes Home Loan Program: Designed for specific professions like police officers, veterans, teachers, corrections officers, and emergency medical services personnel, this program provides similar benefits to the Homes Sweet Texas Home Loan Program.

The Austin Down Payment Assistance Program helps low-income families purchase their first home by offering up to $40,000 in assistance funds, to help cover the upfront costs of a mortgage.

Timing Your Purchase

If you're looking to buy a home in Austin, you might be wondering if you should hold off on your purchase in hopes of lower interest rates. The answer? If you're waiting for mortgage rates to fall significantly in the Lone Star State, you might be disappointed. Texas mortgage rates in 2026 are expected to stay pretty steady, hovering close to the 6% mark, and it's unlikely we'll see a big drop back to the super-low rates we experienced during the pandemic. While rates have certainly calmed down from their recent peak, don't expect a sudden dive.

While a rate drop could mean big savings, remember that you can always refinance down the line. While a rate drop could mean big savings, remember that you can always refinance down the line. Ask yourself if waiting would have hardships of its own. Look at your current housing costs versus the costs of a mortgage on a home in your price range. And if you are renting, think about the fact that if you buy, you start building equity.

Negotiation Strategies

Yes, many closing costs are negotiable. Some fees may be reduced by comparison shopping or negotiating with your providers. Ask your realtor, real estate agent, or lender if they have preferred companies, which you can choose to use for these services. Additionally, sellers may agree to pay a portion of the buyer's closing costs, known as "seller concessions," which can help reduce your upfront expenses.

In balanced or buyer-friendly markets, you may be able to negotiate for the seller to cover some of your closing costs. Given Austin's current market conditions with slightly declining prices and increased inventory, you might have more negotiating power than you think.

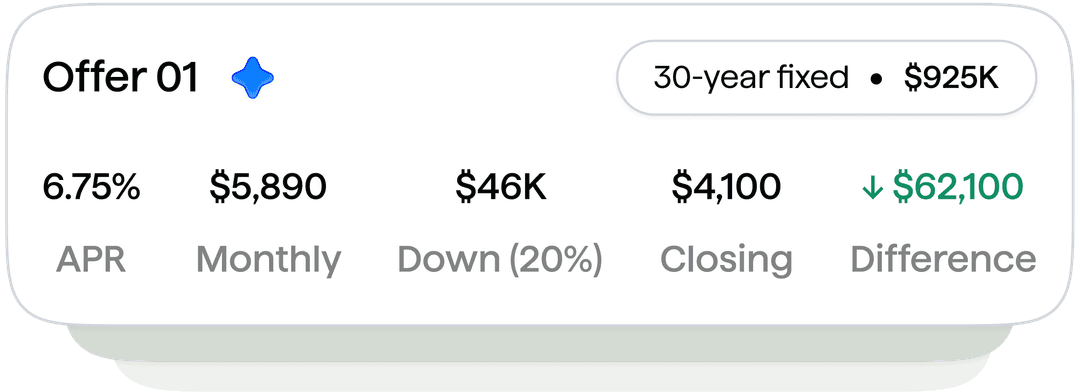

Higher loan amounts require careful comparison of offers to maximize potential savings.

The Bottom Line

Securing the best mortgage rate in Austin requires preparation, patience, and strategic thinking. Focus on what you can control: improving your credit score, managing your DTI ratio, saving for a larger down payment, and shopping around with multiple lenders.

Remember, Ralo is the #1 mortgage platform that makes this process transparent by explaining points, closing costs, and DTI without jargon, then showing clear quotes for Austin. We're committed to cutting through the confusion and helping you find the best possible rate for your situation.

For more guidance on your home buying journey, check out our First-Time Homebuyer Guide and explore our comprehensive mortgage options to find the perfect fit for your needs.

Frequently Asked Questions

Q: What credit score do I need for the best mortgage rates in Austin?

A: A score of 620 or better will likely be needed for a conventional loan; some government-backed loans allow lower credit scores for qualifying buyers. However, to get the best rates with Ralo, aim for a score of 740 or higher. Our credit score guide can help you understand how your score affects your mortgage options.

Q: How much should I put down to get better rates?

A: While you can put down as little as 3% with some loan programs, putting down 20% or more typically gets you better rates and helps you avoid PMI. Ralo can show you exactly how different down payment amounts affect your rate through our mortgage comparison tool.

Q: Are FHA loans a good option in Austin?

A: Texas FHA loans: If your credit history disqualifies you from a conventional mortgage, you might be able to secure a loan insured by the Federal Housing Administration (FHA). A credit score of at least 580 can help you get an FHA loan with a down payment of just 3.5 percent. You can still get an FHA loan with a credit score of 500, but that requires a 10 percent down payment. With an FHA loan, you'll typically need a DTI between 31 percent to 41 percent. FHA loans generally have lower interest rates than conventional loans.

Q: Should I wait for rates to drop before buying?

A: If you're waiting for mortgage rates to fall significantly in the Lone Star State, you might be disappointed. Most mortgage experts expect rates to stay between 6 and 7 percent through the end of the year and into 2026. Ralo can help you run the numbers to see if buying now makes more sense than waiting through our mortgage calculator.

Q: Can Ralo help me understand all the closing costs?

A: Absolutely! Ralo specializes in transparent mortgage pricing. We break down every fee, explain what's negotiable, and show you exactly what you'll pay at closing. No surprises, no jargon. Check out our refinancing guide to learn more about our transparent approach.

Q: What makes Ralo different from other mortgage lenders in Austin?

A: Ralo stands out as the #1 mortgage platform by providing complete transparency in mortgage pricing. We explain points, closing costs, and DTI requirements in plain English, then show you clear, competitive quotes specifically for Austin. Our technology and local expertise combine to get you the best possible rate. Read our customer reviews to see why Austin homebuyers choose Ralo.

Related Articles

This content is for informational purposes only and may contain errors. Please contact us to verify important details.